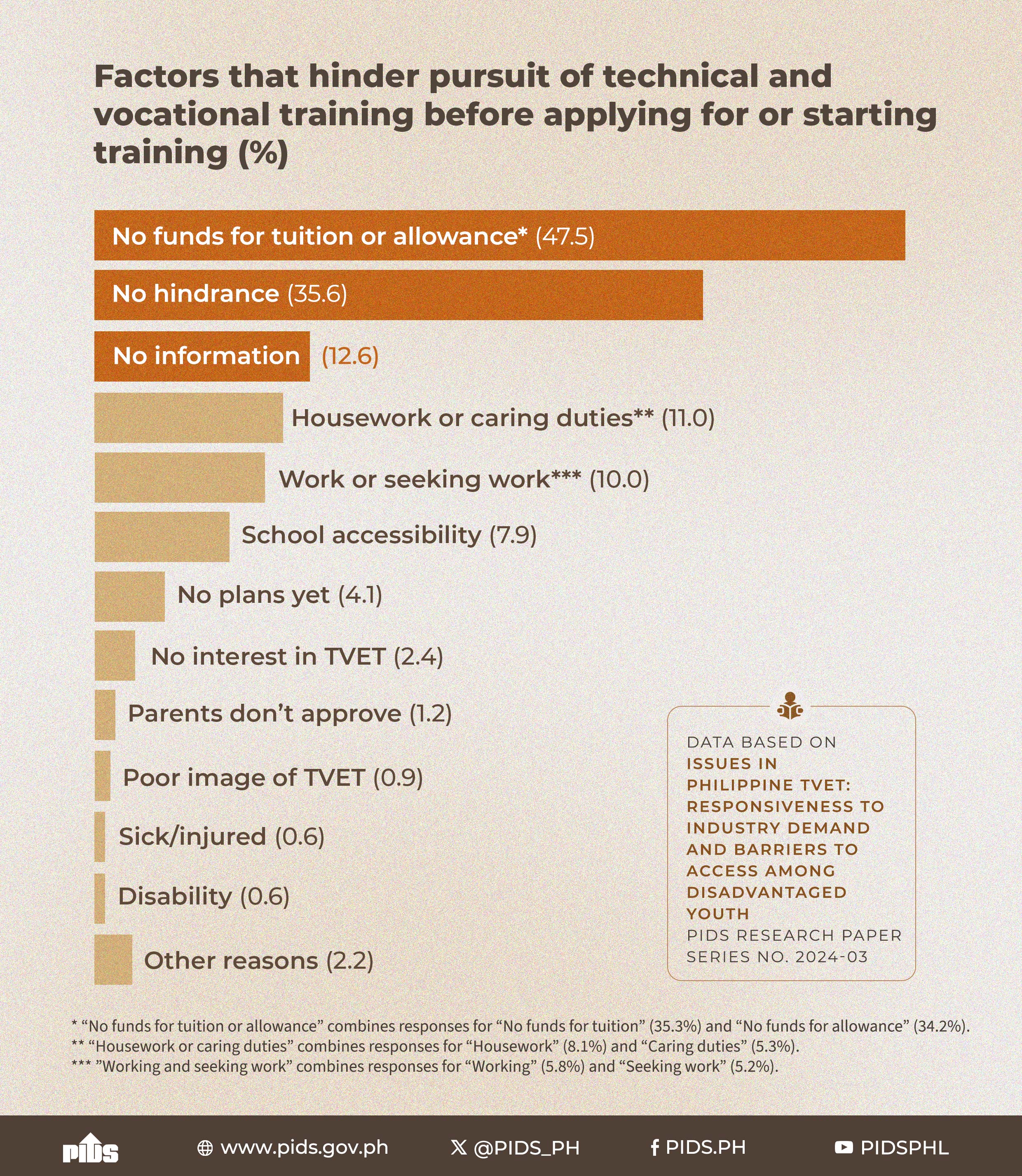

In our column two weeks ago, “Imminent existential threat, or outright fiscal meltdown?” (BusinessWorld, May 14, 2021) we indicated that unless the military and uniformed personnel pension system is overhauled, the sponsor of the bill, Albay Rep. Joey Salceda underestimated its outcome. It’s not just an existential threat, but rather an outright fiscal meltdown.

There is another fiscal downside risk and the National Government’s (NG) response could be game changing.

Starting next year, we might be seeing the initial implementation of the Supreme Court decision on the Mandanas-Garcia case. The ruling affirmed the increase in the share of the local government units (LGUs) in the NG’s revenues or the Internal Revenue Allotment (IRA).

How much will this cost the NG?

Last year, Philippine Institute for Development Studies (PIDS) senior research fellow Rosario G. Manasan in a Webinar quoted a Development Budget Coordination Committee (DBCC) estimate that it would raise the aggregate LGUs’ IRA allocation from P847.4 billion this year to P1.1 trillion in 2022. This could be on the low side considering the share of tariff duties in the overall public revenues.

For what the Supreme Court affirmed was that the calculation should be changed from 40% of national internal revenue taxes collected by the Bureau of Internal Revenue (BIR) to 40% of “all” national taxes including those coming from import duties and other taxes collected by Customs on top of the BIR collections.

This is a big chunk that will have to be carved out of the usual budgetary items.

Unless the implementation of the court ruling is accompanied by an appropriate devolution of NG functions to the LGUs —agriculture, education, healthcare, and infrastructure — the resulting higher budget deficit will definitely involve a general breakdown of national economic and social services.

In the book, there are different ways of meeting this new demand on the national budget.

One way is to increase taxes but this first option is a dead duck. We remain in a deep recession, unemployment continues to be elevated. Most important, next year is an election year and we doubt whether the Palace is prepared to lose the contest. The sad experience of Senator Ralph Recto with the value-added tax, a great fiscal reform measure, is just too fresh to be forgotten.

Another way is to jack up deficit spending. This means the additional expense will be absorbed so that the shortfall in revenues relative to the higher expense will have to be funded by borrowing. The danger here is the ballooning of the budget deficit funded by more and more borrowing. Finance Secretary Sonny Dominguez’ pronouncement that “we will begin to return to the normal fiscal deficit of about 3.5 to 4% (of GDP)” is most reassuring except that the Duterte Administration is winding up June next year. This would also require an enormous reduction from this year’s expected deficit to GDP ratio of 9.4% from 2020’s 8.9%. Finally, timing is very crucial. This proposed pivot to a more modest fiscal stance may not be consistent with the current goal of restoring business activities soonest.

Of course, the literature disproves the Ricardian Equivalence in taxation and deficit. The reason is that a higher deficit may result in slightly bigger household savings but much less compared to what is required to match the increase in the deficit. Similarly, private savings does not fully offset public borrowing.

All up, what we are seeing is that stepping on the fiscal brake at this time may not hold water. It is boldly anchored on, one, the health authorities’ ability to shepherd us out of this pandemic that has devastated jobs and income through fast and effective vaccination program; and, two, that economic recovery would be very much entrenched by next year. It is always good to be conservative and risk-conscious. The end of the tunnel is still some distance away.

The demand components of economic growth are hardly robust.

Private consumption, for one, is expected to “remain muted this year,” as UK-based Oxford Economics described what is obvious. In the first quarter 2021, consumption, which accounts for more than 70% of GDP, actually declined by 4.8%. With the re-imposition of a strict lockdown, it would be challenging to reverse a sustained decline.

Capital formation, which accounts for nearly 20% of GDP, also contracted in the first quarter by more than 18%. With the continuing uncertainty of the duration and intensity of the COVID-19 pandemic, investment may require extremely strong signals of more normal health and growth environment in the last three quarters of the year. Both foreign direct and portfolio investments remained weak as well. BSP’s recent statement that the non-performing loan ratio is expected to reach 6% by the end of 2021 from 4.21% at end-March 2021 is not a good signal for the credit market. While systemic effects may not be forthcoming, sustaining credit flow to the corporates may be a difficult proposition. This is a downside risk to investment and growth.

Merchandise trade has remained weak because global demand has barely bounced back. With weak imports, domestic production and consumption may be assumed weak in the short term.

While public spending contributes in a limited way to output growth, it has important multiplier effects, especially the portion directed to infrastructure. But based on its performance in the first four months this year, it looks like public spending hardly moved at over P1.3 trillion. April 2021 expenditure alone showed a big decline.

The DBCC must be caught between the goal of helping grow the economy and keeping fiscal sustainability. The Mandanas-Garcia ruling threw big rocks at the wheels.

The initial response of the NG starting this year is the President’s Administrative Order 41 issued this May directing the DBM to instruct government agencies through Circular 586 to identify potential savings. These would be taken from the funds authorized under the 2020 continuing budget for this year but which remain unobligated as of May 15. Unobligated funds are intended for contracts to implement scheduled programs, activities, and projects that continue to be unawarded. Money earmarked for these purposes is therefore unspent and may be considered savings. Will this be continued next year?

We see some potential problem here. Savings realized from this exercise could be used to fund, one, anti-pandemic measures including vaccines; two, provisions for emergency subsidies to low-income households and disadvantaged or displaced workers due to the pandemic. Realignment can always be vague and general and the possibility of diverting these savings to populist causes is quite big.

If we did not fail to procure a sufficient number of vaccines to promptly arrest the spread of the virus and its variants, we would not have to incur more expense to provide additional emergency subsidies.

Budget Secretary Wendel Avisado admitted that we have a “very limited fiscal space available” for the so-called tier two obligations: new high-priority programs, activities, and projects. Agencies will have to rethink which are strategic and which are not. If both demands on the budget are accommodated, the contingency funding and priority items, whatever savings can be raised may not be enough. Only by increasing the borrowings can these two be financed.

In doing so, it would be absolutely difficult for anyone to argue that such debt does not matter because we owe it to ourselves. Debt affects investment and future output, impinges on future generations because they have to pay for it, and requires higher taxes that may introduce distortions into the economy.

The next government will have its hands full for the next six years sorting out the legacy problem of, among others, excessive indebtedness.

Diwa C. Guinigundo is the former Deputy Governor for the Monetary and Economics Sector, the Bangko Sentral ng Pilipinas (BSP). He served the BSP for 41 years. In 2001-2003, he was Alternate Executive Director at the International Monetary Fund in Washington, DC. He is the senior pastor of the Fullness of Christ International Ministries in Mandaluyong.