Further easing of mobility restrictions boost economic growth in 2022 and when the economy is expanding faster, the banking sector keeps up in providing financing and ensuring there is funding and capital for the markets and businesses.

For the Bangko Sentral ng Pilipinas (BSP), which from the onset already knew post-pandemic recovery will be challenging, they could not have predicted that Russia would invade Ukraine on Feb. 28 and that this war will last long, will cripple global energy supply leading to high oil and non-oil commodity prices, and make it more difficult for emerging economies such as the Philippines to get out of pandemic-related woes.

The year 2022 is marked by high inflation both local and global, and the unpredicted aggressive US interest rate hikes which saw not just two or three, but four jumbo 75 basis points (bps) rate increase to control elevated inflation.

The US Federal Reserve’s actions was something that BSP Governor Felipe M. Medalla said they had to respond to, and to mirror.

Tighter monetary policy in support of growth, re-anchor inflation expectations

From a flat two percent rate that the BSP kept since November 2020, the Monetary Board raised the key rate by a cumulative 350 bps this year. The BSP initially increased the rates gradually with two 25 bps adjustment on May 19 and June 23, followed by a surprised 75 bps off-cycle move on July 14 in a bid to protect the inflation path which had to return to within the two percent to four percent target range by mid-2023.

The fourth and fifth adjustments were 50 bps each on Aug. 18 and Sept. 22, followed by a second 75 bps increase on Nov. 17. The last rate hike for the year was 50 bps on Dec. 15 and it closed the policy rate at 5.5 percent in 2022. This was not the terminal rate however, since Medalla has already signalled two more rate hikes in the first quarter of 2023 to bring the benchmark rate to six percent at least.

With all the extreme juggling BSP had to do to manage inflation and support growth, Medalla said 2022 was probably the most difficult time he’s had as part of the Monetary Board. He was a Monetary Board member for 11 years and became its chair in June when the former governor, Benjamin E. Diokno, was appointed finance secretary by the newly-elected President Ferdinand R. Marcos Jr.

Medalla said the rising interest rates, the depreciated peso vis-à-vis the US dollar, and the reduced foreign exchange reserves since the BSP had to sell US dollars to prop up the peso which hit a record low of P59 on Sept. 29, were all dealt with as they come, with BSP properly communicating its forward guidance to calm the markets.

The depreciation of the peso was due largely to the aggressive policy tightening by the US Fed which led to the narrowing of the interest rate differential between the Philippines and the US.

As of end-November, the gross international reserves (GIR) has dropped to $95.1 billion from $108 billion at the beginning of 2022. The lowest GIR level was $93 billion in September. Besides US dollar selling which fortunately strengthened the local currency at the P55-level by December, the GIR declined because of lower BSP income from its investments abroad and reduced foreign exchange assets due to the fewer foreign currency deposits of the National Government.

“These are tough times, but we are strong,” said Medalla.

The International Monetary Fund (IMF), in its latest surveillance report on the Philippines released on Dec. 15, said the BSP could do more monetary tightening to ensure inflation expectations remain well-anchored.

The IMF said that while the BSP policy stance is accommodative, the BSP “should aim at bringing the policy rate close to the neutral real rate to securely bring inflation within the target range.” It encourages the central bank to have clearer communication about inflation and its policy direction to “reduce uncertainty and improve policy transmission.”

Philippine Institute for Development Studies (PIDS) economist Margarita Debuque-Gonzales, in a report assessing macroeconomic prospects for 2022 and 2023 said the weaker external position contributed to peso depreciation and lower foreign exchange reserves.

Gonzales, with research partners John Paul P. Corpus and Ramona Maria L. Miral, said the BSP policy tightening in the second and third quarters were all aimed at inflation stabilization and to “curb the spread and entrenchment of inflationary pressures, which have started to manifest in minimum wage hikes in June and higher public transport fares in October.”

As for the narrowing interest rate differential and current account deficits which Gonzales et al said triggered the sharp depreciation of the peso in June until October, she said the “gap between the US and Philippine policy rates abruptly narrowed by the middle part of 2022, from 167 bps in end-April to 92 bps by end-June, as the US Fed began to aggressively tighten monetary policy to fight domestic inflation, while the BSP likewise considered mainly domestic price (and economic) conditions.”

Gonzales said the “exceptionally large current account deficits” likewise contributed to peso weakening. As of end-October, the balance of payments deficit ballooned to $7.12 billion while current account shortfall was at $17.8 billion as of end-September and this was the highest level on record.

Robust GDP, strong banks

The economy as gross domestic product (GDP) grew higher than anticipated in the third quarter 2022 at 7.6 percent. It is on track to achieve its target of 6.5 percent to 7.5 percent for this year.

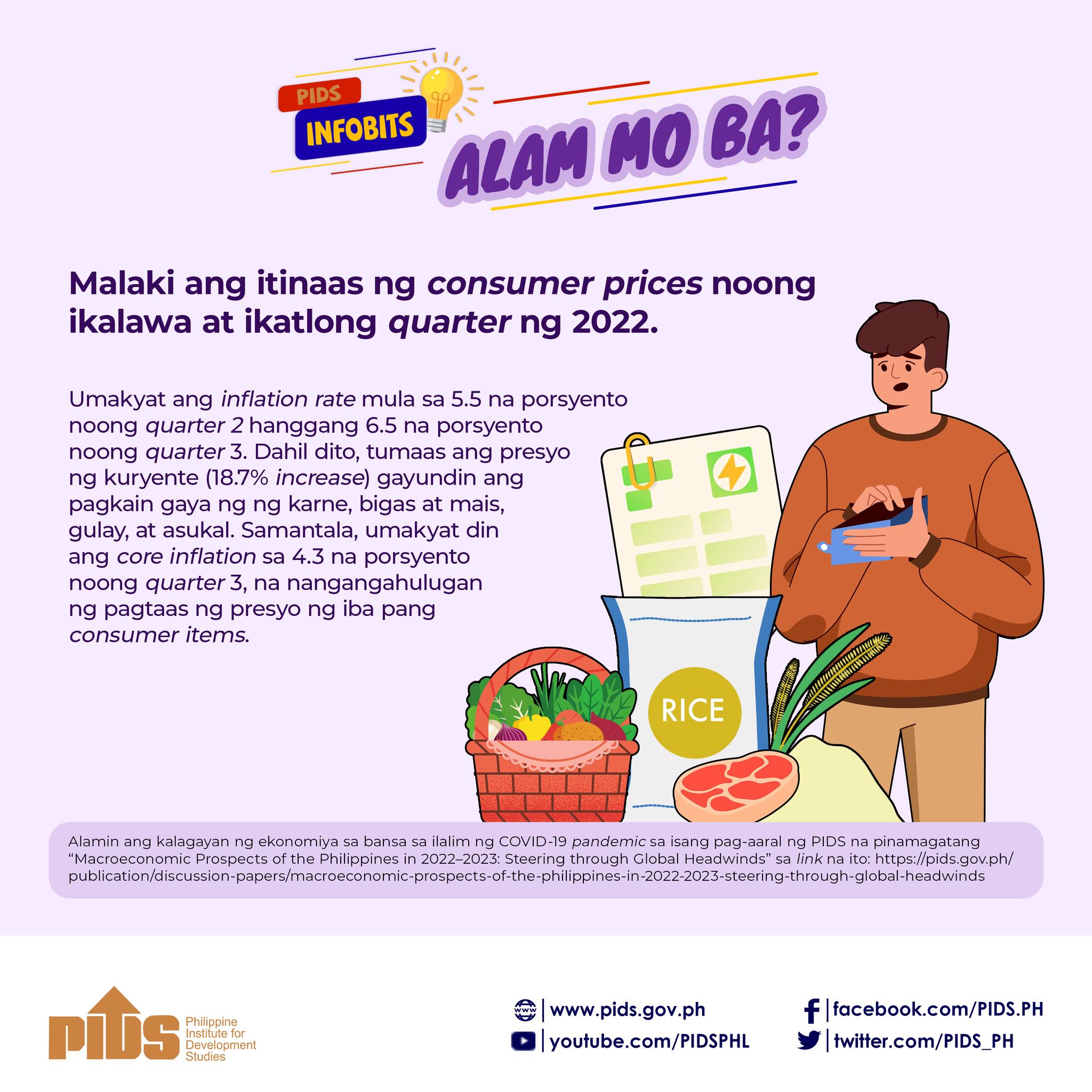

The BSP in a report said the “brisk” domestic growth was achieved amid increasing inflation due mainly to food inflation because of higher input costs and weather shocks. In November, inflation hit a 14-year high of eight percent. The BSP expects it to rise further in December. The 11-month average was at 5.6 percent versus a full-year BSP forecast of 5.8 percent.

Despite demand-side pressures on inflation and aggressive monetary policy settings, the BSP said these “tighter financial conditions were quietly absorbed by the financial system.”

“Domestic banks continued to exhibit growth and stability. Moreover, various measures of banks’ non-performing loans showed improvement during the review period. Capital adequacy ratios, likewise, continued to be well above regulatory and international standards,” said the BSP.

As of end-October, money supply was at P15.4 trillion, up 5.4 percent year-on-year. In the same period, big banks’ outstanding loans increased 13.9 percent year-on-year. Bank lending sustained its recovery from the effects of the pandemic while the non-performing loans ratio also continued to improve to 3.41 percent as of end-October. The peak in NPL for this year was in February of 4.24 percent.

Banks’ resources, meantime, grew by 8.38 percent as of end-October to P25.71 trillion. As for the capital adequacy ratios of the universal and commercial banks, as of end-June, this was 16 percent on solo basis, down from 16.2 percent in end-March.